Auction over, but rollout faces multiple challenges

With the closure of the 5G telecom auctions, India has joined a select list of 70 countries with 5G technology offerings. The government garnered Rs 1.5 lakh crore from the sale of spectrum, with four players bidding actively. At least Rs 13,000 crore of the cash flow is likely this fiscal. From the players’ perspective, subscriber upgrade to 5G and aggressive market share gains will be key to success.

However, 5G rollout faces a host of challenges — among others, a lack of use cases, costly handsets, and potential rollout at a premium that will limit 5G revenue to single digit share of total revenue by fiscal 2026

Additionally, the low level of fiberisation at present will necessitate network capex of Rs 1.5-2.5 lakh crore in the next 2-3 years, with a potential 5-9% increase due to rupee depreciation this fiscal alone. Zero spectrum usage charge (SUC) and relaxation of upfront payment, though, provide some relief here.

As things stand, enterprise readiness is on a sticky wicket at present, though manufacturing appears to be the most suitable and ready for 5G adoption.

We take a closer some of these aspects below.

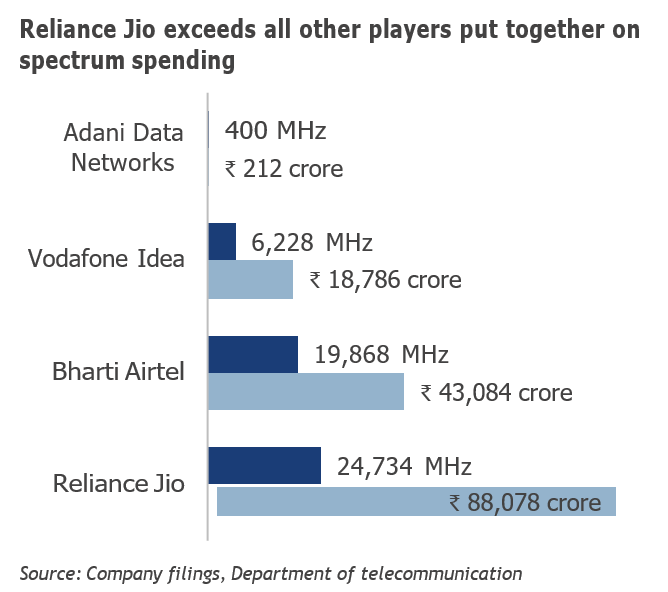

Auction saw some intense bidding

Competition between Reliance Jio and Bharti Airtel was intense. Their spending on the 3300 MHz band in metro and Category A (CAT A) circles — where

deployment is expected to be at an early stage — was on equal footing to acquire equal or more than ideal contiguous bandwidth.

Vodafone Idea’s spending remained at 50% of the top

two players in metro and CAT A circles.

However, Reliance Jio stepped up the game in CAT B and CAT C circles by acquiring 130 MHz in seven out of 14 circles. It spent about Rs 1,500 crore more than Airtel to capture early market share and drive quicker subscriber conversions to 5G, given it has only 4G subscribers.

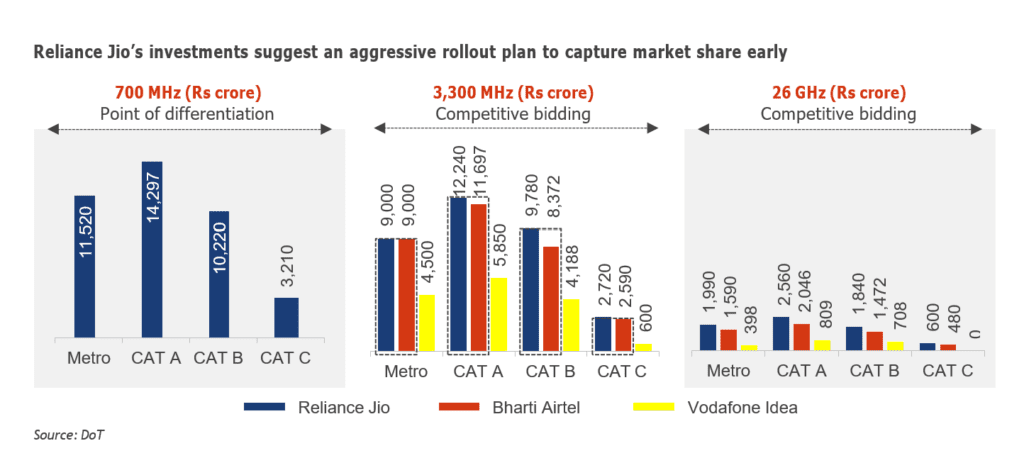

The differentiating factor was 700 MHz

The 700 MHz has always been a premium band as it helps telcos cut costs on towers and provides better network coverage. Due to its low frequency and the ability to penetrate buildings efficiently, the band provides an edge to telcos in terms of connectivity in congested regions.

However, speed is compromised in the 700 MHz band. During test runs, while the top 5G speed of players.

Legacy services, lack of use cases among key hurdles

Sticky usage of legacy services

- ~350 million legacy service users in FY22 despite 11% CAGR fall over FY16-FY22

- These users contribute less than Rs 50 to ARPU and

account for 31% of total subscribers

- Largely spread across CAT B and CAT C

- Conversion from legacy services to 4G/5G data subscribers from legacy to remain crucial

Pricing dilemma and dispersed growth

- Upgrade to 4G from 2G/3G was slow and accelerated

only after tariff wars and heavy data offerings

- Success of 5G hinges on its premium pricing over 4G

- However, reducing price disparity key to faster transition across CAT A and CAT B

- Anticipated 4G tariff hike this fiscal and 5G premium offering in the next will elevate ARPU to Rs 185-190, though it will still be lower than the ARPU of Rs 203 seen in Q4 FY22 for private players in metro circles alone

on mid (3300 MHz) and high (26 GHz) bands was 5-10 Gbps, it plunged to a little over 300 Mbps at a low band such as 700 MHz.

Further, the 700 MHz band is exposed to the risk of low data capacity. A conjugate offering of 700 MHz and 3300 MHz bands mitigates this risk.

The 700 MHz band witnessed interest for the first time with Reliance Jio acquiring 10 MHz across circles at Rs 39,270 crore to rollout pan-India 5G services.

Lack of use cases

- Low penetration of immersive media

- Prices of quality virtual reality handsets range from Rs 2,500 to over Rs 1 lakh, but usage of remains niche

- 4G and existing Wi-Fi technology met the pandemic-induced m-commerce needs

- Growth in interactive shopping, gaming, learning experience critical for increasing penetration

Pricey 5G handset

- The average selling price of smartphones increased by Rs 1,500-2,000 to Rs 14,000- 16,000 in FY22

- Softening demand also slowed production in

April and May 2022

- Share of 5G shipments was low at 15-20% as of FY22

- Elevated 5G mobile handset prices, amid inflationary pressure, could deter subscriber upgrade

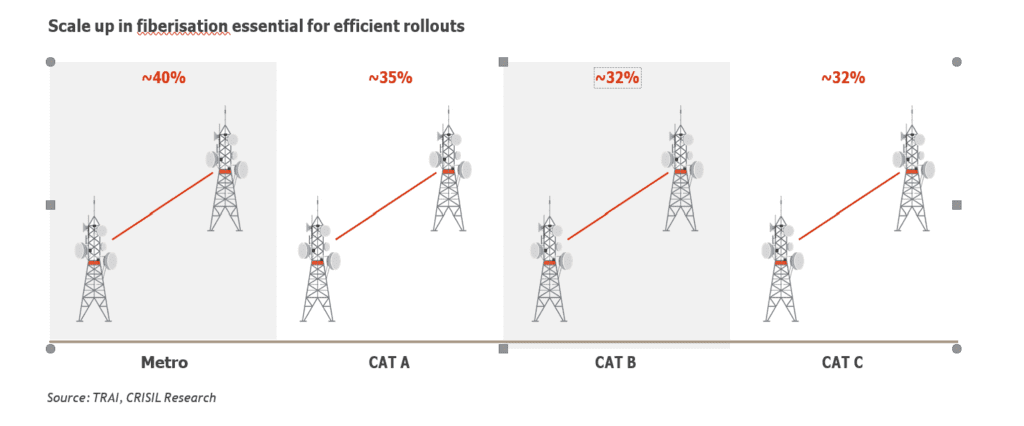

Low fiberisation a key monitorable

metros key for early conversions

The National Broadband Mission targets to fiberise 70% of India’s base transceiver stations (BTS) by fiscal 2025, an ideal requirement for the efficient rollout of 5G services. However, with fiberisation at 35.11% in India as of June 2022, more than 3 lakh km has to be covered at the pan-India level between fiscal 2023 and fiscal 2025. Further, there is a huge variance across states with fiberisation at ~40% in metro and 31-33% in CAT C circles. Fiberisation is less at 25-30% in some CAT B and CAT C circles such as Himachal Pradesh, Uttar Pradesh East and West Bengal. Success of early 4G to 5G conversion hinges on improvement in fiberisation levels in Metros.

A major reason for the slow pace of fiberisation is the right of way (ROW) cost, which ranges from several lakh to a few crore across circles. While the central government has taken efforts to maintain a uniform ROW cost across circles, the high disparity has been a huge roadblock to reaching the fiberisation target.

Telecom operators will have to shell out Rs 1.5 lakh crore to Rs 2.5 lakh crore between fiscal 2023 and 2026 to achieve the remaining 36% fiberisation target by fiscal 2026 and spend on incremental BTS for 5G.

The soaring dollar is also expected to have a marginal impact on the network capex of telecom operators in fiscal 2023. While fiberisation can be achieved through domestic procurement, BTS procurement relies highly on imports (70-75% of the total telecom equipment market).

Despite the government’s Production Linked Incentive (PLI) scheme for telecom and 5G equipment, the reliance on imports for BTS is unlikely to reduce this fiscal. Hence, network capex is expected to grow 5-9% this fiscal due to a high reliance on imports and the appreciating dollar.

Lower upfront payment, zero SUC offer solace

Post collection of ~Rs 1.5 lakh crore and relaxation of upfront payment by 50%, the telecom services operators have an option to pay the dues in 20 instalments.

The outflow towards the first instalment is expected to be at least Rs 13,000-15,000 crore.

Additionally, relaxation of SUC on revenue (weighted average 3% of adjusted gross revenue) realised from new spectrum purchased post-September 2021 is expected to enable cost savings of Rs 3,000 crore

to Rs 5,000 crore for private players. While auction obligations mandate the rollout of 5G services in at least one city by the first year, the full benefit of cost savings is only expected to be realised only in fiscal 2024. Operating margins are also expected to expand a further 150-200 bps.

Enterprise segment is a potential gold mine…

The 26 GHz band is predominantly used for enterprise services in the United States. In India, too, the band is widely accepted for 5G enterprise use cases.

All the players showed a keen interest in the 26GHz band and spent Rs 14,490 crore cumulatively

Reliance Jio led the way with Rs 6,988 crore, followed by Bharti Airtel at Rs 5,588 crore. Despite spending constraints, Vodafone Idea, too, spent Rs 1,914 crore, while Adani Data Networks accounted for the rest.

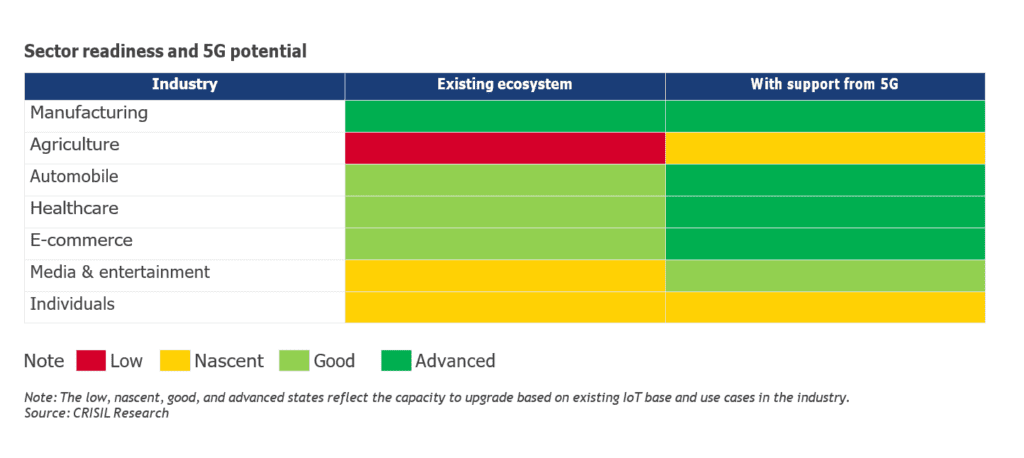

…but industry readiness a point of concern

The readiness level of end-user industries paints a mixed picture.

Barring manufacturing, the existing industrial ecosystem in India is at a rather nascent stage in terms of readiness to adopt advanced 5G technology.

Further, while the pandemic has propelled innovation through digital transformation, the readiness of micro, small and medium enterprises (MSMEs) is even more widely skewed and almost abysmal.

Therefore, the next 2-3 years will be crucial in terms of significant revenue generation based on development of the industrial ecosystem.

The entry of tech players could, however, hamper the 5G revenue prospects of operators.

The global 5G industry, which has grown to account for 2-3% of total revenue in the last 3-4 years, is also mired in similar issues, made worse by the pandemic and competition, leading to soft 5G launches.

India, on the other hand, is likely to be in a better shape, given adequate availability of handsets and other technology infrastructure in the global market. However, the above-mentioned roadblocks are expected to limit the share of 5G revenue in total Indian telecom revenue to single digit till fiscal 2026.

{kind=link}

{kind=link}

{kind=link}

{kind=link}